Subsidies for "green hydrogen" may give platinum a replacement market for catalytic converters. But it is a money pit that threatens the long-term economic stability of the Cape

In the past few months we have had a fair bit of noise from the platinum sector about structural decline in demand, due to the replacement of demand for carbon-fuel vehicles with electric ones. See, the old cars use catalytic converters, which need platinum, which the new electric vehicles don’t.

Just the last week, we’ve had Northam CEO Paul Dunne tell Reuters that the sector is in terminal decline. The Minerals Council VP spelled out the same doomsday scenario to the Shanghai market, while overall growth starts to take a slow dive.

But the industry has not entirely given up. As Martin Creamer said recently, covering this sector on his Mining Weekly podcast:

“What the platinum group mining industry is planning, is to try and stimulate demand. They see that the best way of doing this is by stimulating interest in green hydrogen. Now we see that the green hydrogen is produced with electrolysers that need platinum group metals […] you then pass that through a fuel cell to create clean electricity and that fuel cell also requires platinum group metal. On both sides of the equation, you have got demand coming in and that is what they want to emphasise at the moment.”

And lo’ and behold, just as the Platinum sector starts to cry, the European Union swoops in with a magical windfall (though predictably enough, the EU got off its press release a full two days before the South African government did).

Not being a corporate analyst myself, it’s hard to tell exactly what the past few months’ fluctuation in share prices mean, but it does seem odd for the industry to send out alarm bells on the airwaves just as the EU prepares to hand them a life raft.

Though on the other hand, it surely adds a bit of pressure to up the subsidy, since South Africa’s political stability has a major global impact, and our political stability has long depended on the mining sector’s healthy performance.

Resource hogging

But this is a resource-intensive business. The process requires 9-10 litres of fresh water for every gram of hydrogen. That is a terrible idea for an industry in a place as water-scarce as South Africa.

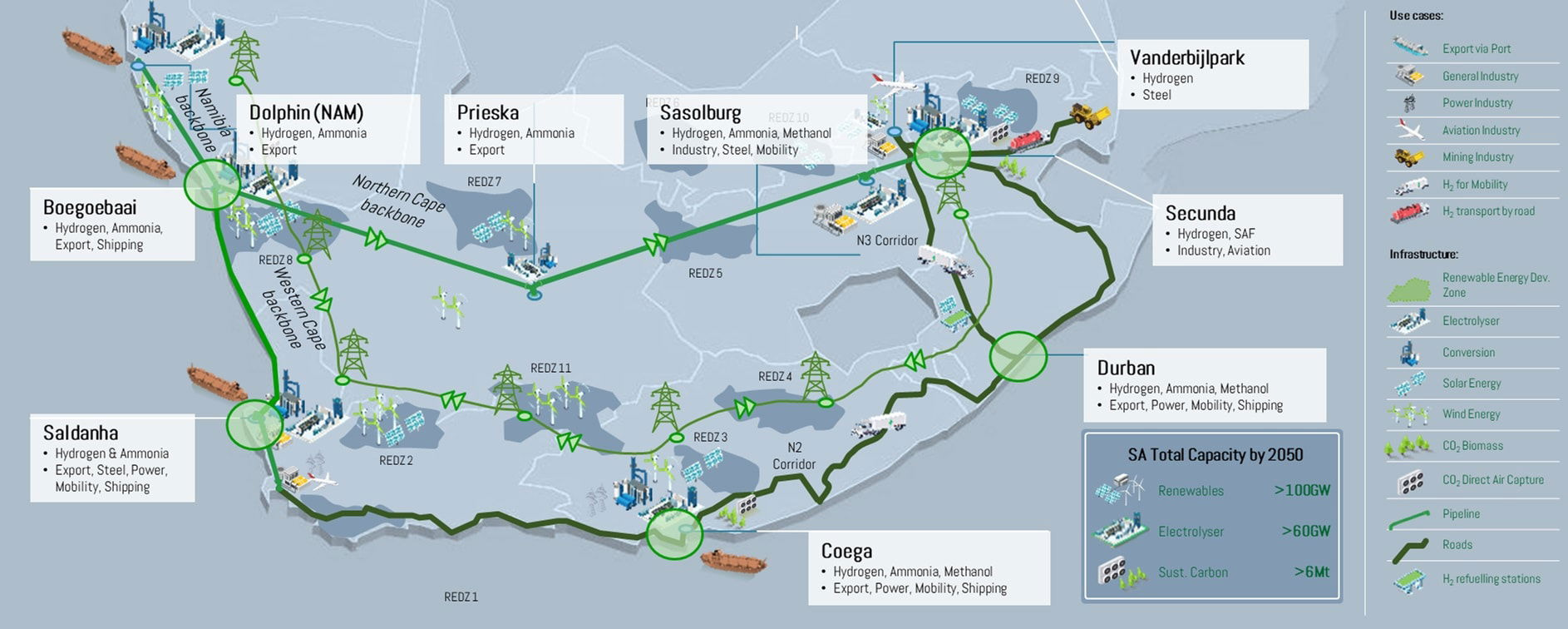

But it gets worse, because the main projects currently under way are not even in the wetter parts of our country, but in the arid zones of the Cape, whose water security is in no way secure, and came within months of a humanitarian catastrophe during the dry spell in 2018. The first major green hydrogen project is going to be a major corridor running from Saldanha through the Northern Cape to Namibia, who equally foolishly, wishes to become some sort of hub for hydrogen.

The Dutch subsidised development program, called the Green Hydrogen Fund, is naturally, in its South African concern, also a BEE project, designed in collaboration with Alan Winde’s good friends at WESGRO. Press on this fund promise $1 billion (roughly R18 billion) for this endeavour. Another R105 billion is being dumped into the Coega Special Economic Zone by Hive Energy UK.

But the broader plan, which brings in the SADC as a regional partner, is much broader in scope, and encompasses the entire country:

The new EU deal, according to the World Bank, will require “around 1.6 gigawatt (GW) of renewable energy […] to produce 50,000 tons of green hydrogen annually, which is equivalent to 280,000 tons of green ammonia. Out of the estimated capital expenditures of around $2 billion, 66 percent is allocated to investments in solar farms and wind turbines. These investments are crucial for obtaining the "social license” for green hydrogen, adding affordable generation capacity to the energy grid.

And just coincidentally, the Western Cape government just commissioned 1.5GW of methane-driven energy generation in that very location. So not only will this divert water resources, but a significant chunk of the new power generation capacity we have built to fix loadshedding.

Money pit?

But what exactly is green hydrogen? Being that my father is a chemical engineer who has worked in several different energy sectors, I get to tap him for resources on this stuff every now and then. Plus there’s always Hugo Kruger, whose writing is a consistently decent source for the layman to peek around the corners of industry PR and government green grift.

The reason hydrogen is a crap fuel source comes down, not to limitation imposed by present technological conditions, but by physical laws themselves, As Kruger puts it:

“While all technologies experience learning curves and adhere to an equivalence of Moore’s Law, which revolutionised the semiconductor industry, it is important to remember that ultimately, learning curves are constrained by the laws of physics. This is why internal combustion engines haven’t significantly improved in fuel efficiency in over 40 years, why the supersonic concorde was never economically viable and why certain sceptics argue that battery electrical vehicles might not see mass adaptation for the middle income groups. One simply cannot squeeze blood out of a rock.”

Kruger suggests the use of synthetic fuels to replace traditional fossil fuels. This means syn gas, a technology developed by SASOL in the old days to get around oil sanctions, which uses a combination of fossil fuel exhaust products (carbon monoxide and hydrogen) to produce cleaner carbon fuel sources. This, he argues, is much better than investing in the overexpansion of the electrical grid to cope with the wild fluctuations of power provided by wind and solar, which require massive battery storage, long-distance transmission, and curtailment (dumping generated power).

But fundamentally, the limit is physics itself:

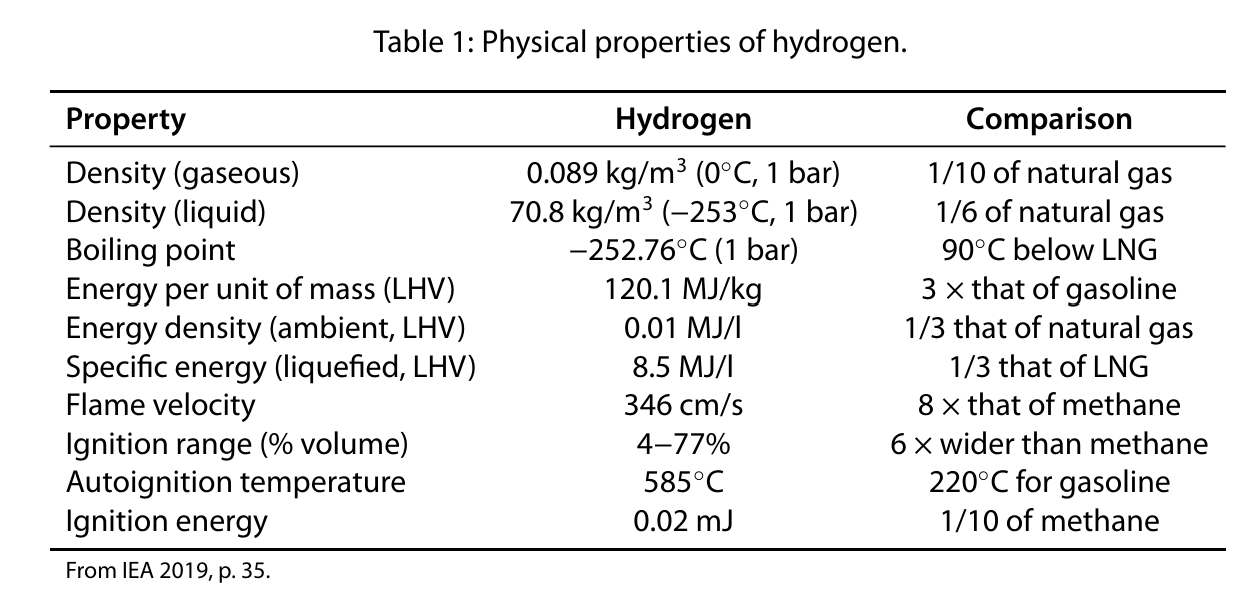

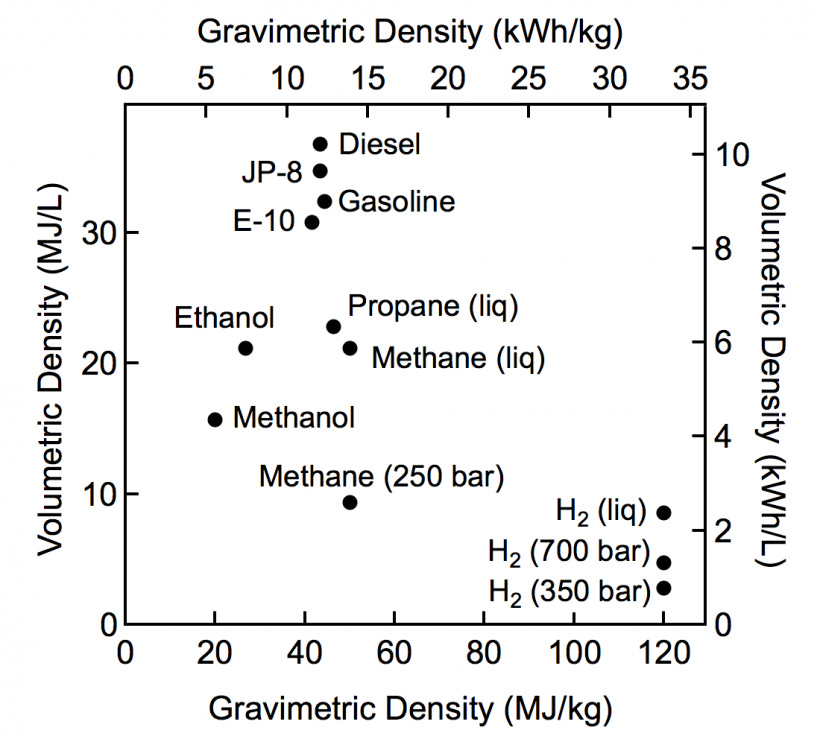

What we see here, is that hydrogen is not nearly energy-dense enough to make up for the enormous costs of using it as an energy-storage medium. It is really bulky, and cannot be condensed enough to justify its use. Worse, splitting it off from green sources (electrolysing water) is such a massive cost that it becomes, once one takes the whole supply chain into account, an almost worthless source of energy.

Both Kruger and my dad independently pointed me to the analysis of Michael Liebreich, who cheerfully points out that hydrogen simply is not efficient, safe, or convenient.

The vast majority of hydrogen used in any industry (mostly as a chemical feedstock for making fertilisers and petrochemicals) is from hydrocarbon sources itself. So what the “green” hydrogen is, is that expensive electrolysis process mentioned above.

Predictions about the price of hydrogen dropping to rates competitive with traditional fuel sources, Liebreich claims, are woefully oversold. The big figure Liebreich chucks out here is that 70%-86% of the energy from the electricity that goes into storing hydrogen is lost by the time the hydrogen is used as a fuel source itself. And as Liebreich says here, saving the best for last, is that even in the case of “white” hydrogen, freely obtained from ground sources, the transport and storage costs are prohibitive of any market competitiveness without massive subsidies.

In short, the entire sector is a massive energy sink. In every category, hydrogen costs more - more to produce, transport, store, distribute and use - than any other energy source, not just in dollars, but in energy costs.

The general idea behind pushing new tech with subsidies is that by increasing production, one can drive up technological efficiency, and eventually get it to a sustainable level.

But in the case of green hydrogen, it’s just not possible. It only exists as an industry because of massive subsidies, and loans motivated by wildly inflated expectations of future efficiency.

Qui bono?

Aside from the silliness of the Western green subsidy market, which is ideologically deranged, corrupt, and pointless for the most part, at the very least, there will be a temporary employment opportunity, and some easy money for the big state-adjacent players.

But one sliver of the South African market does have something to benefit. Our platinum mining sector has been dumping money into green hydrogen for a long time, and believes very earnestly in the future of hydrogen as an energy source.

One major source of optimistic projection here is the inauspiciously named Mordor Intelligence, which claims that the new green tech will lead to a 4.47% increase in the price of platinum group metals between now and 2029. Whether this is mere PR or not, the sector has already been investing heavily.

At the height of loadshedding, hydrogen fuel cells were a flagship feature in the mining sector, as an on-location alternative to slower and less reliable sources like solar or wind. While other fossil fuel sources would be more cost-effective, building one’s own power plant is a bureaucratic nightmare, and mining companies know a fair bit about this, seeing as the average time for the turnaround of a mining license in South Africa is a round ten years.

As this old M&G article from 2015 shows, the Chamber of Mines was extremely excited to expand the use of platinum into a new market as the EV revolution first loomed, and the scarcity of electricity at the time made this make sense - our deep mineshafts are so unlivable without modern powered ventilation that any power outage poses a severe threat.

They even threw some crumbs to a local rural village in free electricity to check some equity boxes with the state.

But the big reason behind the keenness for this technology is that it uses platinum.

The platinum sector is generally in trouble, and in a chronic sort of way. The price of platinum, which once soared above $2,000 an ounce, has plunged to $939—marking a 13% drop since last year. This decline, exacerbated by falling demand for catalytic converters in traditional vehicles, spells trouble for an industry that heavily depends on the automotive sector.

Northam Platinum’s fortunes have waned in parallel with these market shifts. The company reported an 81.6% drop in headline earnings per share for the year ending June, down to 4.45 rand ($0.25) from 24.15 rand the previous year. The broader sector has been similarly afflicted, with palladium prices down 40% in 2023 and rhodium trading at a fraction of its 2021 peak.

The South African platinum sector, once a global powerhouse, has been in steady retreat. Output peaked at 5.3 million ounces in 2006 but has since dwindled. Dunne forecasts a further 10% drop in production over the next five years, from the current 3.9 million ounces to around 3.5 million. He expects Northam’s production to stabilize at approximately 1 million ounces annually, a target bolstered by increased output from its Eland mine.

So what is to be done?

The best way to save the platinum sector would be to pour R&D funding into the metal’s use in battery technology.

Platinum Group Metals, a dual-listed entity in New York and Toronto, is making strides in South Africa's Waterberg region, where it aims to revolutionize battery technology with palladium and platinum. The Japan Organisation for Metals and Energy Security has also thrown its weight behind the Waterberg project by establishing HJ Platinum Metals, a special-purpose holding company.

Traditionally absent from the battery electric vehicle (BEV) market, if the new technologies being developed here make headway, it could change the future of the country's mining sector by ameliorating the impact of the global decline in demand for catalytic converters.

The intensive drive to integrate palladium and platinum into lithium battery technology is spearheaded by Lion Battery Technologies, a venture jointly established by Platinum Group Metals and Anglo American Platinum. Lion's ambitious target is to produce batteries with specific energies 20% to 100% higher than current technologies, all while maintaining or exceeding existing cycle lives.

The Waterberg project, situated in the Bushveld Complex's northern limb. The project is designed as a mechanised, shallow mine extracting palladium, platinum, gold, and rhodium. The company is advancing towards a development and construction decision, with a recently approved $1.35-million budget for stage-four work programmes, a part of a larger two-year, $21-million pre-construction plan.

In parallel, a cooperation agreement has been established with Ajlan & Bros Mining and Metals to explore the creation of a standalone PGM smelter and base metal refinery in Saudi Arabia. This study aims to diversify the sources of PGM concentrate, reducing the risk associated with reliance on a single project.

But as for the hydrogen, it’s just hot air.